Student debt — and how to pay it off

Like the majority of American students, Brooks-Long had to borrow money to pay for her degree, which she acquired from Baylor University, a private school.

But with no access to federal student loans due to a family issue around a contested inheritance, Brooks-Long had to turn to private funding from Sallie Mae.

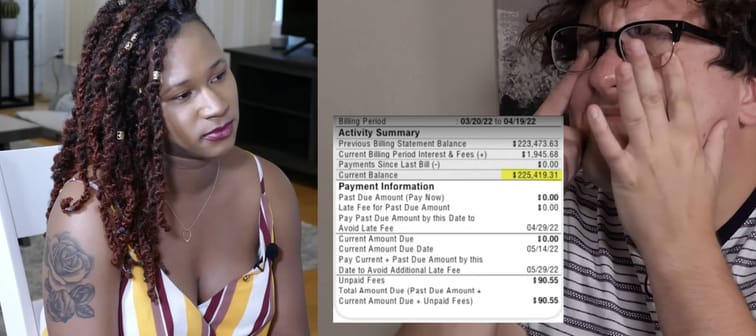

She took out three student loans worth about $176,000, but her debt swelled to nearly $250,000 with interest and fees.

At the time she spoke with Hammer, her bill between May and April of 2022 was $1,945 — more than two-thirds of her income of $2,816, which she was bringing in working four jobs.

“It's going to be a million dollars before she knows it,” Hammer told Insider of Brooks-Long’s terrifying tale of student debt.

Brooks-Long is not alone in struggling with student debt. Today, Americans owe a combined $1.7 trillion for their education.

There are a few things you can do to reduce your student debt or pay it off faster. If you have private loans, like Brooks-Long, you can attempt to refinance them to try and secure lower interest rates. Remember that it’s worth shopping around and comparing quotes from multiple lenders before selecting the option that best fits your needs.

If you have a federal loan, you won’t be able to refinance, but you could switch over to an income-driven repayment plan, which would allow you to make more affordable payments based on what you earn.

Kiss Your Credit Card Debt Goodbye

Having a single loan to pay off makes it easier to manage your payments, and you can often get a better interest rate than what you might be paying on credit cards and car loans.

Fiona is an online marketplace offering personalized loan options based on your unique financial situation.

When you consolidate your debt with a personal loan, you can roll your payments into one monthly installment. Find a lower interest rate and pay down your debt faster today.

Get Started

Avoid mistakes that will ruin your credit score

When Brooks-Long sought Hammer’s advice, the interest rate on her three private student loans was 11.75% on the two larger ones and 9.875% on the smaller one of $37,000.

In comparison, the interest rate for all new federal direct undergraduate student loans for the 2023-24 school year is 5.50%.

Brooks-Long didn’t share how her student loans are structured, but Hammer told Insider he hoped she didn’t have a variable interest rate on her loans because the amount she owed would have increased due to repeated rate hikes.

In addition to her student loan struggles, Brooks-Long — who is trying to make it as an actress in San Antonio — shared with Hammer how she fell into credit card and car loan debt.

A year before meeting Hammer, she took out a $13,500 auto loan, which costs her $300 a month, and by the time she spoke with the YouTuber she’d paid multiple late fees already.

When asked about her credit score, she found it had taken a big hit — from 720 to 549 — since acquiring the auto loan.

Hammer recommended she sell her car: “You literally cannot afford this car,” he told her. “You cannot sell your credit card and pay it off. You cannot sell your student loans and pay it off. You can sell your car.” But she insisted it wasn’t as big a problem as her student debt.

Brooks-Long also carried a balance on her credit card and admitted to overdrafting on her checking account multiple times a month.

“That is just dire,” Hammer told Insider. “That's where it gets to the point where it feels like it's impossible to get out of.”

All of these common financial mistakes can damage your credit score and leave you in poor standing if you need to borrow more money. Not only that, they can limit your options to getting out of debt — keep in mind that whether you qualify for refinancing will depend a great deal on your credit score.

Boost your income

Brooks-Long took on multiple jobs to pay off her debts, including working as a virtual assistant for a realtor, an enrollment advisor for an online university, at an ad agency and modeling and acting gigs.

But ultimately, she was spending almost double what she was bringing in. Hammer said she needed to earn double or even triple her income in order to pay off her “ballooning” debts.

“If you don't, you're not going to be able to do anything for the rest of your life,” he told her.

There are multiple ways you can supplement your income. For example, you could look for a new job that offers a higher salary.

If you want to boost your income without switching jobs, or you're able to work beyond the average 40-hour week, consider taking on multiple gigs like Brooks-Long.

You could also earn some extra cash by selling items online, renting out some space (a room or even a parking spot) or getting a housemate who can split some of your housing costs.

Brooks-Long actually did this — splitting her bills with her roommate, who is also her cousin — but this backfired as she often ended up paying more than her fair share because her cousin was unemployed.

Hammer went on to advise Brooks-Long stick with a strict budget, which included no more eating out even if she needed to travel for work.

“Pack a sandwich,” he said.

Sponsored

Follow These Steps if you Want to Retire Early

Secure your financial future with a tailored plan to maximize investments, navigate taxes, and retire comfortably.

Zoe Financial is an online platform that can match you with a network of vetted fiduciary advisors who are evaluated based on their credentials, education, experience, and pricing. The best part? - there is no fee to find an advisor.