Titan Invest review: hedge-fund style investing for $100

FellowNeko / Shutterstock

Updated: January 02, 2024

We adhere to strict standards of editorial integrity to help you make decisions with confidence. Please be aware that some (or all) products and services linked in this article are from our sponsors.

We adhere to strict standards of editorial integrity to help you make decisions with confidence. Please be aware that some (or all) products and services linked in this article are from our sponsors.

If you want to invest like a hedge fund, you might think that you need millions of dollars or to have the right connections.

However, companies like Titan are working to change this. This actively-managed investing platform invests like hedge funds, aiming to outperform the market to maximize returns for investors.

Granted, this unique investing approach isn't for everyone, and higher fees come with the territory. Our Titan review is covering how this innovative company works, what the pros and cons are, and how to decide if it's right for you.

Pros & cons

Pros

- $100 minimum investment requirement

- Open to non-accredited investors

- Variety of investing strategies

- Short-selling can provide some downside protection

- Crypto investing is available

- Titan has expanded into other investing sectors like real estate

Cons

- Higher fees than most robo-advisors or ETF investing

- Limited performance history, especially for newer strategies

- Titan Cash doesn't pay as much interest as some savings products

Who is Titan for?

Investors who are comfortable with more risk for higher potential returns are Titan's customers. This actively-managed investing platform seeks to outperform the market.

To accomplish this goal, Titan invests in small groups of stocks or cryptocurrencies, so you don't get the same level of diversification you do with ETF investing. This strategy, compounded with short selling for downside protection, is how Titan is different from its competitors.

What makes Titan great?

Titan is actively managed, and the company tracks what major hedge funds are buying and selling by using SEC filings and invests in similar companies. The company also hedges investments by shorting a percentage of your portfolio depending on your risk tolerance. That way, some of your portfolio still benefits even if markets go down, which is how hedge funds operate.

These practices are why Titan is like a hedge fund, although the company stresses how it's neither a hedge fund nor a robo-advisor.

This investing style is also what makes Titan unique. You get an actively managed fund that's similar to hedge funds without the requirement of investing millions of dollars or being an accredited investor.

Multiple investing strategies

Titan currently has seven different strategies you can invest with:

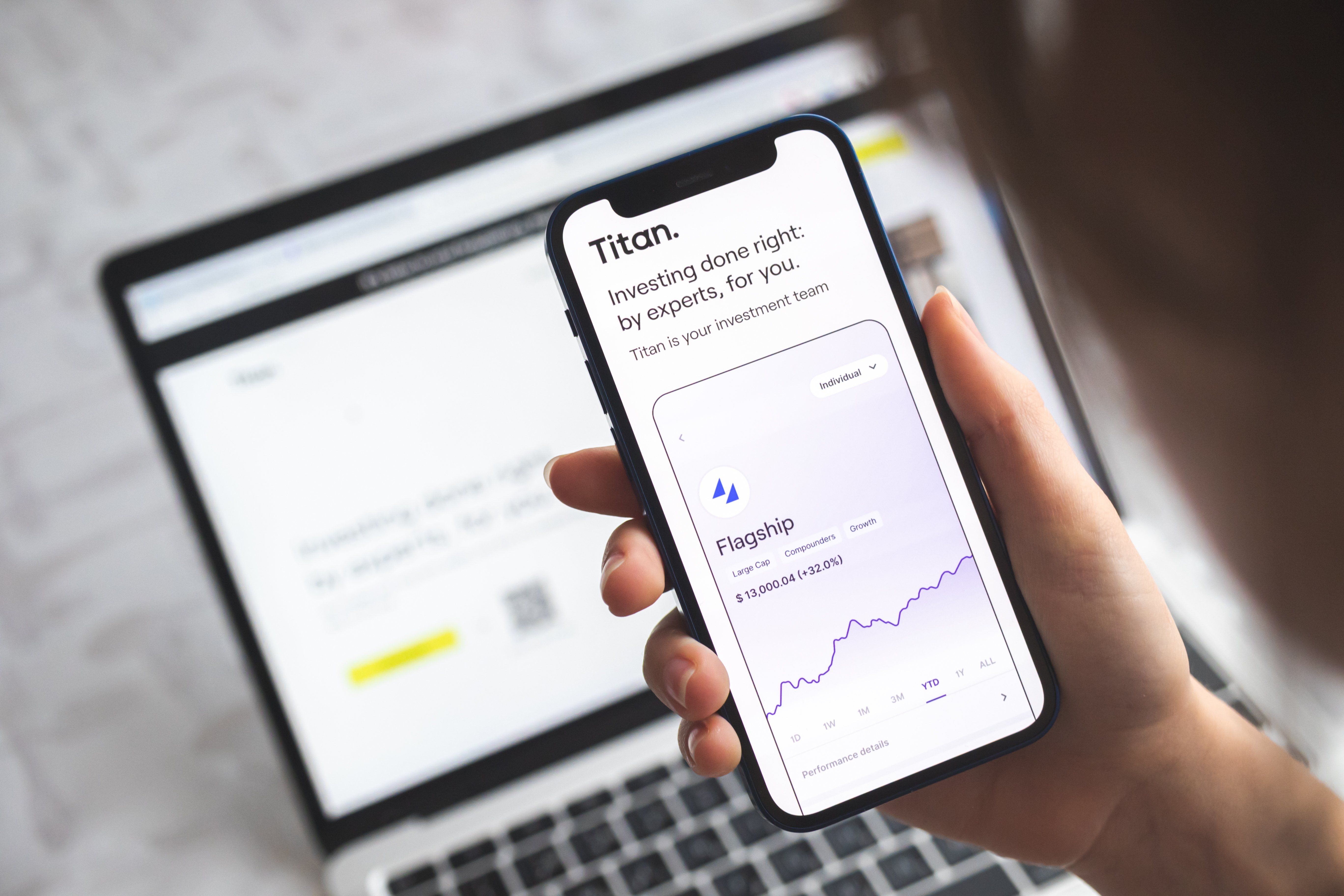

- Flagship: Titan's first portfolio that's comprised of large cap U.S. companies. This portfolio aims to outperform the S&P 500 and includes some of the largest U.S. companies.

- Opportunities: Includes smaller U.S. companies with more growth potential.

- Offshore: An international-only portfolio that invests in developing markets like China and Latin America.

- Crypto: Titan's crypto fund invests in approximately 5 to 10 major cryptos.

- ARK Venture Fund: This fund partners with Cathie Woods ARK Invest to invest in a portfolio of approximately 40 publicly traded companies in a VC-style mandate.

- Apollo Diversified Real Estate Fund: The goal of this fund is to generate income and capital appreciation through private real estate funds and public real estate securities.

- Tactical Private Credit Fund: This fund aims to produce income by using Carlyle's Global credit platform to invest in a range of credit types.

You can invest with one or several Titan strategies. And its website shares more information about historical performance and holdings for some of its main strategies:

One downside is that there's a limited track record for all the strategies. This is especially true for ones that launched recently, like the ARK Venture Fund.

Flagship and Opportunities strategies have strong returns within the last few years, while Offshore is dreadful. And while Titan Crypto began in a bull market, crypto winter has seen this portfolio lose over 50% of its value at the time of writing.

However, having multiple options is still an advantage since you can diversify your portfolio with these different strategies. And since Titan actively managed funds, it also uses practices like quarterly portfolio rebalancing and tax-loss harvesting to help maximize returns.

Hedged investments

One unique aspect of Titan is that it provides downside protection through hedging for its equity strategies. The company shorts a certain percentage of your portfolio depending on your risk tolerance. Because of these short positions, you can potentially still earn profits even if the market declines.

Hedging is why hedge funds have their name. The main appeal of this strategy is that it helps limit the impact of market volatility and helps investors generate returns consistently.

Funnily enough, many hedge funds actually fail to outperform index funds or the S&P 500. Warren Buffett famously proved this after winning a decade-long bet that passive investing would beat most hedge funds. But many investors don't mind this fact because of the downside protection and potential for more consistent returns.

Titan claims hedging is the reason it was ranked the #1 investment advisor out of 60+ others for equity returns during Covid 19, although it doesn't state where this ranking came from.

Titan Crypto investing

Titan's newest strategy is crypto, and this is a benefit if you want to add digital assets to your portfolio but don't know where to start.

Many robo-advisors and funds are still behind on true crypto investing. Sure, they might invest in funds like the Grayscale Bitcoin Trust, but they aren't buying altcoins or really diving into crypto.

In contrast, Titan Crypto is a basket of 5 to 10 coins that the team believes are positioned for long-term returns. Essentially, these are cryptos that Titan thinks will still be market leaders within the next 3 to 5 years. Titan also considers factors like liquidity, regulatory concerns, and overall risk versus reward when determining asset allocation.

And Titan is going for large-cap cryptos, not random altcoins that are unproven. This includes obvious choices like Bitcoin and Ethereum as well as promising coins like Cardano and Solana.

You still get way more control and selection if you use a crypto exchange like Coinbase or Gemini to trade. But the fact Titan has an actively managed crypto fund is fairly unique.

Low investing minimum

You only need $100 to invest with Titan. This is slightly higher than most online stock brokers that have a $0 minimum. But it's still an excellent way to invest with little money, which you wouldn't expect from an actively managed fund.

Note that Titan Opportunities and Titan Offshore require $10,000 to start investing.

Titan Cash

One new Titan investing strategy you can use is Titan Cash. This lets you earn 2% APY on your idle cash if you invest at least $1,000 with Titan. You earn the 2% rate up to $10,000, after which point your interest rate drops to 0.50%. Your money also gets up to $250,000 in FDIC insurance.

This rate isn't as high as many high-yield savings accounts on the market. And robo-advisors like Wealthfont have Wealthfront Cash that lets you pay bills and earn a higher APY at the time of writing. But Titan didn't always have a cash management account type of offering, so this is an upgrade to the platform.

Available accounts

You can invest through individual taxable accounts or retirement accounts like traditional, Roth, and inherited IRAs. It also supports 401(k), IRA rollovers, and 403(b) accounts.

Fractional shares

Another advantage is that it supports fractional shares. This lets you put all of your capital to work so you don't have heaps of idle cash sitting on the sidelines.

This is also important since strategies like the Flagship portfolio invest in major, large cap U.S. companies where stock prices can be hundreds or thousands of dollars.

No lock-up period

Titan doesn't require locking in your money, and you can withdraw funds anytime. Withdrawals take 2 to 4 business days on average, so liquidity isn't a concern.

What are Titan's drawbacks?

In a crowded market of robo-advisors and online brokers, Titan is quite different. It's not a hedge fund or robo-advisor, but rather an actively managed fund that borrows ideas from both sides.

However, despite its more unique investing approach, Titan isn't without some drawbacks.

Missing Some Asset Classes

One advantage of using robo-advisors like Betterment or Wealthfront is that you can invest in portfolios that have other asset classes like bonds and even mutual funds in some cases. In contrast, Titan just sticks with equities and, more recently, crypto, private credit, and real estate.

The trade-off is that Titan should have higher returns on average than portfolios with a high bond concentration. But having the flexibility to choose between safer fixed-income investments and equity investments might appeal to some investors.

However, Titan's continued expansion of its investing strategies has made the platform much more robust than when it first launched.

Annual Management Fees

Titan charges $5 per month on accounts with assets under $10,000 and 1% annually if you have over $10,000 in assets. It doesn't charge performance fees like hedge funds, but paying 1% annually is high versus most robo-advisors.

For example, Betterment and Wealthfront each charge 0.25% annually; four times lower than Titan.

Granted, Titan is actively managed, but factor in the higher fees when deciding if it's worth it.

Limited historical performance

One of the main downsides of Titan is that its portfolios have limited track records. And this is apparent when you look at funds like Titan Crypto. The highly-anticipated fund boasted over 300% in annualized returns shortly after launching, but these days, the average annualized return rate is about -50%.

That's still an excellent rate of return for many investors, but it shows how short time periods can dramatically change the numbers.

Titan fees and pricing

Titan has two different pricing models depending on your total account balance:

- Under $10,000: Pay $5 per month.

- Over $10,000: Pay 1% in annual management fees.

Note that Titan considers the total value of your assets under management, not individual accounts. So, if you have $5,000 in a Titan Flagship portfolio and $10,000 in Titan Crypto, you pay 1% on the total balance, not $5 on the Flagship account and 1% on the Crypto account.

How to contact Titan

You can contact Titan by emailing support@titan.com. You can also message customer support through Titan's Android and iOS app.

Is Titan safe and secure?

According to its website, Titan protects your personal and financial information by using SSL and 256-bit encryption. It's also registered with the SEC, and accounts get up to $500,000 in SIPC insurance. Overall, this makes Titan safe and secure, and it follows similar practices as other FinTech companies.

The company also states that it would sell off all securities and return funds to clients in the event it shuts down. However, know that all investments carry some degree of risk and that Titan doesn't guarantee future performance or that your portfolio can't decline in value.

Best alternatives

If you want hedge-fund style investing and believe in active management over passive investing, Titan is an excellent choice. Few options on the market use shorting as a form of downside protection, and the $100 minimum investment requirement means anyone can realistically get started with Titan.

That said, Titan's main drawbacks are its limited performance history and the 1% annual management fee. If you want longer-standing companies and lower fees, we think robo-advisors are a better choice.

Here's how Titan compares versus alternatives like Betterment, Empower, and Wealthfront.

| Highlights | Empower | Betterment | Wealthfront |

|---|---|---|---|

| Rating | 4.8/5 | 4.5/5 | 4.5/5 |

| Minimum to open account | $100,000 | $10 | $500 |

| 401(k) assistance | ✅ | ✅ | ❌ |

| Two-factor auth. | ✅ | ✅ | ✅ |

| Advice options | Automated, human assisted | Automated, human assisted | Automated |

| Socially responsible investing | ✅ | ✅ | ✅ |

| Learn more | Sign up | Sign up | Sign up |

| Review | Empower review | Betterment review | Wealthfront review |

For example, Betterment is our favorite robo-advisor, and it has a $0 funding requirement. And with 0.25% for annual fees, it's more affordable that Titan. You also get access to more portfolio variety, including ones for socially responsible investing and fixed-income.

Wealthfront is also an excellent alternative since it's low-fee. There's a $500 minimum requirement, but Wealthfront also gives you more control over the ETFs that are in your portfolio.

Finally, Empower is a comprehensive wealth-management tool that's ideal if you have over $100,000 to invest. It's not actually a robo-advisor, and you get access to human advisors through its wealth management service. There's a 0.89% annual fee, which is still less than Titan and cheaper than many financial advisors. Plus, the platform has plenty of free tools like a retirement planner and investment fee analyzer that are useful.

To be clear, Titan invests differently than these platforms because of how it mirrors hedge funds and uses shorting for downside protection. If this style is what you're looking for, go with Titan. But for lower fees and passive investing, robo-advisors or companies like Empower are superior.

Bottom line

It's not quite a hedge fund, and it's definitely not a robo-advisor. But Titan is an exciting and different option for investors with some promising strategies.

Only time will tell how Titan's strategies play out versus overall market returns and more passive investing. It's shown early signs of success for some funds, and poor returns in others. However, with a $100 minimum and short selling that's tailored to your risk tolerance, it's the best way to invest like a hedge fund without having a lot of capital.

Moneywise receives cash compensation from Wealthfront Advisers LLC (“Wealthfront Advisers”) for each new client that applies for a Wealthfront Automated Investing Account through our links. This creates an incentive that results in a material conflict of interest. Moneywise is not a Wealthfront Advisers client, and this is a paid endorsement. More information is available via our links to Wealthfront Advisers.